First Home Guarantee Expansion - What It Means for First Home Buyers (and Where Mondus Fits In)

For many Australians, the dream of owning a first home has felt increasingly out of reach. Rising property prices, slow wage growth, and the challenge of saving a deposit have created what feels like an impossible equation: you can afford the repayments, but you can’t get past the upfront deposit hurdle. It takes an average of 11 years to save for the average home deposit, and up to 16 years in Sydney.

In welcome news, the Federal Government has brought forward the expansion of the First Home Guarantee (FHG) to October 1, 2025. Originally slated for January 2026, this change gives first home buyers earlier access to the scheme’s new, more generous rules.

But what does the expansion mean in practice? And how does it compare to alternatives like Mondus’ shared equity model? Let’s unpack the details.

What Is the First Home Guarantee?

The First Home Guarantee is a government initiative that helps Australians purchase their first home with as little as a 5% deposit. Traditionally, buyers putting down less than 20% must pay Lender’s Mortgage Insurance (LMI), which can add tens of thousands of dollars to the cost of a mortgage. Under the FHG, the government essentially “guarantees” the loan, allowing lenders to waive LMI.

The result: first home buyers can enter the market sooner, with lower upfront costs.

What’s Changing From October 1, 2025?

The expansion is significant and addresses some of the program’s long-standing barriers. Here are the highlights:

- No more income limits: Previously, singles and couples had to fall under strict income thresholds to qualify. These restrictions are gone, meaning higher-earning Australians can now access the scheme.

- No more property price caps: Buyers were once constrained by price limits that often fell well below actual market conditions, especially in Sydney and Melbourne. These caps have been removed.

- Unlimited places: The scheme was once capped at 35,000 places per year. From October 2025, that limit disappears - anyone who qualifies can apply.

- No LMI: The removal of LMI for 5% deposit buyers remains one of the program’s biggest savings drivers.

- Broader lender panel: More regional and customer-owned banks are joining the scheme, increasing access for buyers outside metropolitan hubs.

Why the Change Was Brought Forward

The government’s decision to move the start date forward by three months (from January 1, 2026 to October 1, 2025) was driven by urgency. With affordability continuing to dominate headlines, policymakers wanted Australians to have earlier access to the new, more flexible scheme.

For first home buyers who’ve been waiting on the sidelines, this is an immediate green light.

What It Means for First Home Buyers

At first glance, this expansion looks like a game-changer. And for some, it will be. Buyers who earn above the old income thresholds or who were boxed out by property price caps will now be eligible. Plus, the removal of the cap on places removes the “race to apply” dynamic that frustrated many in previous years.

However, it’s important to remember that the FHG is still a traditional lending model. Buyers must borrow 95% of the purchase price through a participating bank. This means taking on a significant debt load and relying on lenders’ criteria for approval.

The scheme reduces upfront costs but doesn’t avoid the need to save for a deposit, which is still a hefty feat on top of rising cost of living. For example for a $700,000 home you’ll need $35,000 in savings, plus more to cover stamp duty and other settlement costs. Including stamp duty and settlement costs you’ll need in the order of $50,000 - $80,000 in savings to buy a $700,0000 home, depending on the state.

It’s definitely a big step forward but doesn’t solve the problem for the growing percentage of good income earners who don’t have a deposit.

.png)

How Mondus Compares

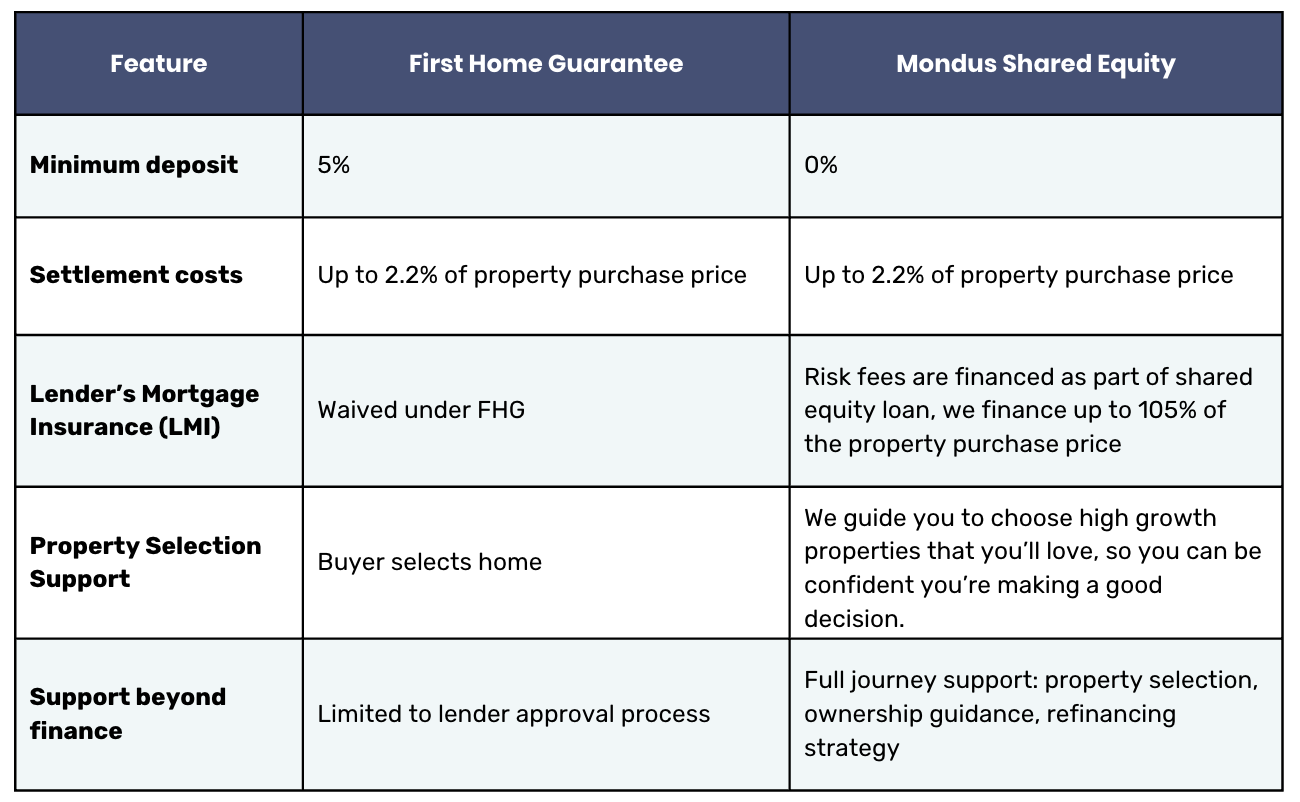

- This is where Mondus’s 0% desposit shared equity model comes in Like the FHG, Mondus is designed to solve the deposit problem but it does so in a very different way. In fact, we’re able to solve the deposit gap completely. In a nutshell: With Mondus, there is 0% despot, compared to 5% under the FHG.

- We finance 100% of the property value in a single blended loan with competitive interest rate.

- You own the property outright, we’re not on title.

- You contribute up to 2.2% of the property value as a contribution towards settlement costs - conveyancing, title search, pest and building inspections, legal and admin costs that you’ll have to pay for any property.

- Mondus’s incentives are aligned with the buyer’s success. Mondus only benefits if the property grows in value and the buyer successfully refinances into full ownership.

- Property selection is powered by AI-driven analysis and tailored for owner-occupiers, helping ensure buyers choose a property with strong fundamentals, so you can build equity sooner

- Buyers receive ongoing support, from purchase through to refinancing - a level of handholding that banks simply don’t provide.

Here’s a side-by-side snapshot:

Which Option Is Better?

This isn’t a question of which option is better; it depends on the buyer’s circumstances.

- For some, particularly those who have access to a 5% deposit and are comfortable taking on a 95% loan and who can meet banks’ criteria, the FHG will be an attractive route.

- For others, especially those who don’t have a deposit and are looking for expert property guidance, Mondus may be the smarter path.

What’s most important is that buyers now have more options. The expansion of the FHG puts housing affordability in the spotlight, but Mondus ensures that those still left behind by traditional lending models have another way forward.

Join us at Mondus Capital

We’re not just financing homes—we’re reimagining the framework of property investment and ownership. Take the first step towards owning your dream home today, with Mondus Capital guiding you every step of the way.

Previous articles

First Home Guarantee Expansion - What It Means for First Home Buyers (and Where Mondus Fits In)

First Home Guarantee Expansion vs Mondus 0% Deposit Loan: What Buyers Need to Know

Top 5 Common Home Loan Mistakes First-Time Buyers Make

Avoid the common mistakes first-time home buyers make when applying for a home loan. Learn how to improve your chances of success with these expert tips.

6 trending suburbs to buy in Perth for first home buyers

Liveability: what makes a suburb the right choice for you?

Affordable housing solutions for Gen Z—will they be able to afford a home in Australia?

Unlocking affordable housing solutions: how Mondus will help 1,000 Australians buy homes without a deposit